A Rail Turnaround

Destini has already delivered 3 quarters in the black after aggressively kitchen sinking in 18M24 (ended June), that saw heavy impairments and exit/disposal from problematic segments/subsidiaries.

Stock information

Destini Berhad

DESTINI - MYX 7212

BUY

Target price: RM0.65

Last price: RM0.40

Market cap: RM220m

Shares out: 549m

52w range: RM0.20 / RM0.42

3M ADV: RM0m

T12M returns: 33%

Disclaimer: By using this information, you acknowledge that you are solely responsible for evaluating the merits and risks of any investment decision and agree not to hold NewParadigm Research liable for any damages arising from such decisions.

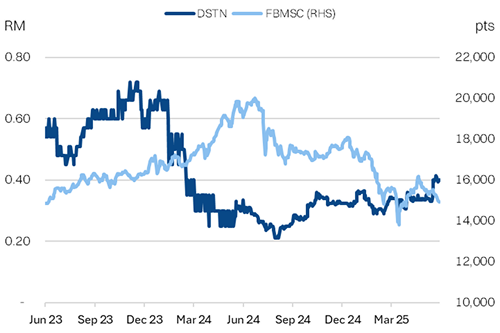

Share Price Performance

Investment Fundamentals

| RMm | 18M42A | FY25E | FY26E2 | FY27E3 |

|---|---|---|---|---|

| Revenue | 159.3 | 340.5 | 454.4 | 499.8 |

| Revenue growth | 54% | 114% | 33% | 10% |

| EBITDA | -119.1 | 47.6 | 61.3 | 71.2 |

| EBITDA margin | -75% | 14% | 13% | 14% |

| PATAMI | -140.1 | 30.6 | 40.4 | 47.4 |

| Adj PATAMI | -60.9 | 30.6 | 40.4 | 47.4 |

| EPS (sen) | -70.4 | 6.1 | 8.1 | 9.5 |

| DPS (sen) | - | 0.5 | 2.4 | 2.8 |

| ROA | -23% | 10% | 8& | 9% |

| ROE | -53% | 20% | 21% | 20% |

| PER | - | 6.7 | 5.1 | 4.3 |

| P/BV | - | 1.4 | 1.1 | 0.9 |

| Yield | 0% | 0% | 1% | 6% |

| Net debt/Equity | -26% | -27% | -42% | -41% |

Source: Bloomberg, NewParadigm Research, 2025

Key Points

- 785m orderbook driving +32% YoY upside to FY26E NP,underpinned by a major MRO job for KTMB.

- Tenderbook of RM3.2bn, with estimated ~RM430m

≥70%probability of winning; ~RM100m of potential contract awards in thecoming 1-2months. - Long shot: aiming for a 25-year refurbishment and leasing contractworth RM5bn; RM200m revenue per year.

We initiate coverage on Destini Bhd with a BUY and target price of RM0.65, which implies a 64% upside. Even without any multiple expansion, Destini’s ~32% YoY earnings growth for FY26 should drivet he fair value of the stock to RM0.54. However, we anticipate further contract wins coupled with a gradual dispelling of negative legacy perception, justifies a moderate re-rating to at least 8.8x PER.

- Quality earnings growth: We forecast a step up in earnings to RM40m for FY26E (+32% YoY), underpinned by steady execution of the MRO contract for KTM (RM570m outstanding). We anticipate upside potential to our assumptions, pending variation orders to scope ofwork. Note, management is guiding for FY26E earnings of ~RM50m.

- New contract wins: We believe Destini should trade like a construction stock going forward and enjoy re-rating in valuations in line with new contract wins. The group has a bid book of RM3.2bn, of which at least RM433m is high probability (≥70% chance of winning) and another RM485m with 50%-70% chance. Management is guiding for~RM100m in contract awards to be decided in the next 1-2 months that will be a ST catalyst for the share price.

- Long shot: Destini is also pursuing a high upside but low-probability leasing contract from KTMB worth potentially RM4-5bn over 25years. MoT has pivoted strategically towards a leasing model for rolling stock assets, creating the opportunity for Destini to acquire old rolling stock, refurbish it, and lease it back. The key challenge for Destini, is the up-front capex heavy nature of a leasing business.

Destini has already delivered 3 quarters in the black after aggressively kitchen sinking in 18M24 (ended June), that saw heavy impairments and exit/disposal from problematic segments/subsidiaries. The group has also recapitalised substantially (led by an RM60m injection by the major shareholder/chairman) and should be able to fund further growth without another cash call on shareholders. To underscore this point, management is guiding for a 0.5 sen dividend per share for FY25 and potentially introducing a dividend payout policy of at least 30% going forward.

Valuation

We value Destini at an undemanding 8.8x FY26E PER. This compares favourably at -1.7xStd Dev against the pre-2018 average PER of 21x.Initiate coverage with a BUY.

About Destini

About the company

Destini Bhd offers engineering services in mobility (mostly rail), aviation and defence (primarily for the military), marine (for O&G) and energy (predominantly solar. The bulk of Destini’s operations are based in Malaysia, but it has a small footprint in Singapore, China. Australia and UAE. The bulk of Destini’s orderbook today relates to the maintenance, repair and overhaul (MRO) of KTMB rolling stock.

About the Stock

Destini Bhd offers engineering services in mobility (mostly rail), aviation and defence (primarily for the military), marine (for O&G) and energy (predominantly solar. The bulk of Destini’s operations are based in Malaysia, but it has a small footprint in Singapore, China. Australia and UAE. The bulk of Destini’s orderbook today relates to the maintenance, repair and overhaul (MRO) of KTMB rolling stock.

Thesis and risks

Investment thesis

Destini is a turnaround story, that is still building credibility. As the profitability track-record continues and the group continues to build its orderbook, the market should reward the company with a smaller discount on valuations. Critically, the stock has virtually no institutional ownership, for now. Destini’s profits for the next 2-3 years are underpinned by its Level 4 MRO contract with KTMB (RM695m), and new contract wins are supported by a sizable RM3.2bn bid book funnel.

Key risks

Political risk – Destini primarily contracts with the government or government linked entities. Changes to the political establishment can be disruptive to contract flows and payments, as seen in 2018.

Cash flow risk – Despite turning profitable, Destini’s bloating receivables has translated persisting cash flow drag and remains reliant on debt.

Cyclical risk – Destini has enjoyed lumpy level 4 MRO contracts, but such overhaul/refurbishment cycles are irregular and infrequent – likely more so as RAC moves towards a leasing model.

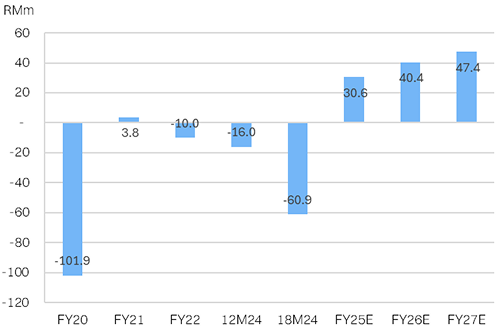

Chart 1: Adjusted PATAMI outlook

Getting Destini back on track

Initiate with BUY; RM 0.65 target price

Destini has been off investors’ radar for some time, and for good reason. The group has been struggling to break even since Pakatan Harapan took over the government in 2018, which precipitating significant disruption to Destini’s defence contracts.

But we think Destini is worth revisiting. The group has been profitable for the past 3 consecutive quarters, as the turnaround plan implemented by Datuk Abd Aziz Haji Sheikh Fadzir (Chairman, major shareholder) is beginning to take shape.

The key change, has been the recapitalization of the group (with RM60m from Datuk Aziz himself), shedding of problematic subsidiaries, and some cost-rationalization. This included almost ~RM150m in provisions and impairments in the extended 18M24 (ended-June; change in FYE).

The stronger balance sheet is allowing Destini to execute the RM695m in maintenance, repair and overhaul (MRO) projects for 45 total trainsets via its 70%-controlled subsidiary M Rail Technics S/B. (RAILTEC; balance 30% by KTM Bhd):

May 2022: RM531m MRO contract for 35 six-car-sets: (Link)

Sept 2022: RM164m MRO contract for 10 electric train sets: (Link)

Notably, Destini’s valuations did not re-rate on the news of the aforementioned contract awards, perhaps overshadowed by the group’s weak balance sheet and persistent losses. However, with Destini now turning a profit, we think markets should begin reflecting the turnaround going forward, especially if there are more contract wins.

The MRO projects in hand are contributing ~RM4m/qtr to Destini’s PATAMI or about 50% of the mix over the past nine months, bringing Destini’s 9MFY25 PATAMI to RM19.7m. This implies the group is trading at an a mere 7.8x trailing annualised PER. However, management is guiding for RM30m in PATAMI for FY25E, which then implies a mere 6.7x trailing PER.

Looking ahead, we think Destini should be able to accelerate earnings to RM40m for FY26E, which implies a forward multiple that is only 5.1x. By any measure, cheap. Note, that management’s own forecasts are more bullish – aiming for RM50m earnings for FY26E. This will hinge on timely execution (MRO contracts only payable on delivery of rolling stock, including passing certification) as well as securing variation orders on out-of-scope work.

Even holding the current trailing multiple unchanged. Destini should be valued at

RM0.54. But we believe the company can trade at a less discounted multiple of at least 8.8x forward PER, on the basis that it should have a stream of new contract awards to announce.

In turn, we initiate coverage on with a BUY recommendation and a target price of

RM0.65 based on a target multiple of 8.8x FY26E PER.

The catalysts

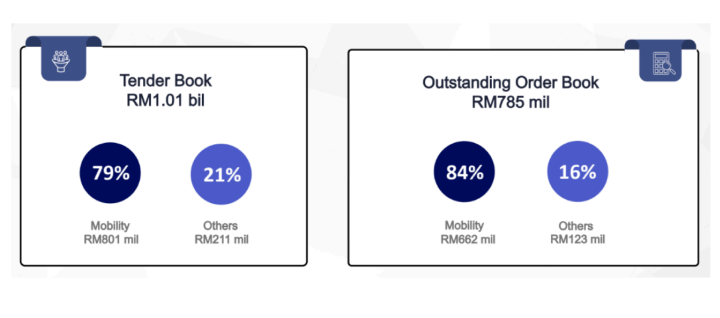

With a healthier balance sheet and a growing profitability track-record, we anticipate that Destini’s share price should be more reactive to new contract wins going forward – not unlike a construction stock. To this end, Destini has a bid funnel of RM3.2bn. Management advertises a tenderbook of RM1bn, with an implied win rate of ~34%. Note that bid figures in this section are gross, not adjusted for minority stakes.

Of the funnel, the most immediate catalysts could materialize in the next 1-2 months with management is guiding that an estimated RM100m worth of its active bids should be awarded – both for rail sector related contracts – for which management has indicated a high-degree of confidence in securing.

- Estimated RM60-70m Level 3 MRO contract for 9 ETS; from MOT (Link).

- Estimated RM20-30m MRT related MRO contracts.

Looking ahead, we think it is worthwhile scrutinizing Destini’s tenderbook. Management

is guiding for a tenderbook of that is roughly 79% mobility-driven:

Chart 2: Destini’s tenderbook and orderbook.

However, it is worth noting that the tenderbook is heavily skewed by a large rail project with a low-probability of success. We think a more accurate depiction of the tenderbook profile by probability of success. In this approach we find Destini has ~RM433m worth of high- probability bids (>70% chance of success) and RM485m worth of moderate probability bids (50-70% chance of success).