Destini Berhad

DESTINI - MYX 7212

Stock information

Destini Berhad

DESTINI - MYX 7212

BUY

Target price: RM0.65

Last price: RM0.40

Market cap: RM220m

Shares out: 549m

52w range: RM0.20 / RM0.42

3M ADV: RM0m

T12M returns: 33%

Disclaimer: By using this information, you acknowledge that you are solely responsible for evaluating the merits and risks of any investment decision and agree not to hold NewParadigm Research liable for any damages arising from such decisions.

About Destini

About the company

Destini Bhd offers engineering services in mobility (mostly rail), aviation and defence (primarily for the military), marine (for O&G) and energy (predominantly solar. The bulk of Destini’s operations are based in Malaysia, but it has a small footprint in Singapore, China. Australia and UAE. The bulk of Destini’s orderbook today relates to the maintenance, repair and overhaul (MRO) of KTMB rolling stock.

About the Stock

Destini Bhd offers engineering services in mobility (mostly rail), aviation and defence (primarily for the military), marine (for O&G) and energy (predominantly solar. The bulk of Destini’s operations are based in Malaysia, but it has a small footprint in Singapore, China. Australia and UAE. The bulk of Destini’s orderbook today relates to the maintenance, repair and overhaul (MRO) of KTMB rolling stock.

Thesis and risks

Destini is a turnaround story, that is still building credibility. As the profitability track-record continues and the group continues to build its orderbook, the market should reward the company with a smaller discount on valuations. Critically, the stock has virtually no institutional ownership, for now.

Destini’s profits for the next 2-3 years are underpinned by its Level 4 MRO contract with KTMB (RM695m), and new contract wins are supported by a sizable RM3.2bn bid book funnel

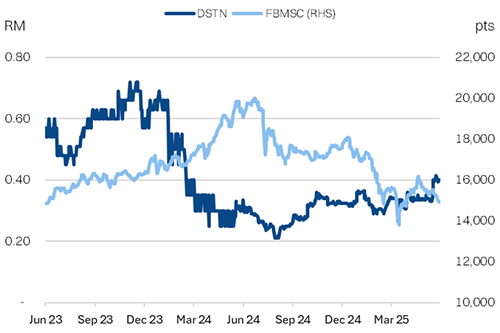

Share Price Performance

Destini has been off investors’ radar for some time, and for good reason. The group has been struggling to break even since Pakatan Harapan took over the government in 2018, which precipitating significant disruption to Destini’s defence contracts.

But we think Destini is worth revisiting. The group has been profitable for the past 3 consecutive quarters, as the turnaround plan implemented by Datuk Abd Aziz Haji Sheikh Fadzir (Chairman, major shareholder) is beginning to take shape.

The key change, has been the recapitalization of the group (with RM60m from Datuk Aziz himself), shedding of problematic subsidiaries, and some cost-rationalization. This included almost ~RM150m in provisions and impairments in the extended 18M24 (ended-June; change in FYE).

The stronger balance sheet is allowing Destini to execute the RM695m in maintenance, repair and overhaul (MRO) projects for 45 total trainsets via its 70%-controlled subsidiary M Rail Technics S/B. (RAILTEC; balance 30% by KTM Bhd)